In a previous blog, we discussed the exorbitant cost of drugs, even generics and the tactics that the pharmacy industry employs to keep the costs high. Well, as the 1974 Bachman Turner Overdrive hit song goes, “You Ain’t Seen Nothing Yet!”

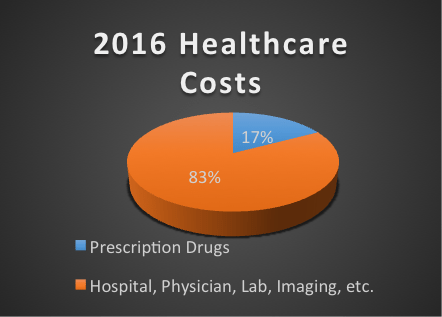

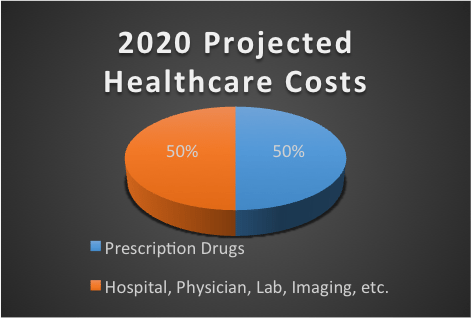

Over the past few months, having participated in over a half-dozen health insurance meetings, carrier broker advisory panels and most recently listening to the President of the nation’s largest Pharmacy Benefit Management company, there is unanimous agreement that by late 2019 or sometime during 2020, pharmacy spend in a health insurance plan will account for 50% of the healthcare pie. That is a dramatic increase compared to the current level at 14% to 17% for most plans.

That doesn’t mean that all other healthcare expenses will remain static. No, they will increase as they have historically, at two to three times the current rate of inflation.

Besides the tinkering and price gouging by the pharmaceutical industry described in the previous article, what keeps the health insurance industry thought leaders up at night? The proliferation of specialty drugs. Specialty drugs are a class of pharmaceuticals that treat a specific disease and are allowed to proceed on a fast track for FDA approval. They can be both and injectable or an oral medication. Because they treat a disease or symptom that doesn’t have a large number of diagnoses, they have a dramatically higher price tag versus standard medications. Here are a few examples of the annual retail cost of some specialty drugs:

Arthritis: Enbrel® $48,000 (up 80.3% since 2013) and Humira® $44,400 (up 68.77% since 2013);

Hepatitis C: Harvoni® $94,500 and Sovaldi® $84,000;

Oncology: Eight approved by August 2016 sixteen in the pipeline through 2017. Cost estimates are $125,000 to $500,000 per course of treatment;

Muscular Dystrophy: Exondys 51® $300,000 (This drug’s approval was initially rejected by the FDA but extreme political pressure to approve this drug even though initial clinical trials didn’t show any significant improvement in MD patients. This pressure caused the FDA to reverse its decision and allow the drug’s use with an ongoing random control study.)

This isn’t even the tip of the iceberg. So far this year and over the next two years alone there are dozens of new specialty drugs in almost every area of medical practice receiving approval, many costing hundreds of thousands of dollars per year or course of treatment. Even more concerning is that many of these drugs have biologic formulations which are nearly impossible to duplicate even after a patent expires giving the drug company a virtual lifetime monopoly on the drug.

Increasing prescription costs are affecting all aspects of health insurance delivery, from private insurance companies, to Medicaid for the poor, to the VA for our veterans and Medicare for our senior population. Medicare Trustees recently reported that their trust funds will be completely depleted two years sooner than previously projected (in 2028 versus 2030) with pharmaceutical costs being the primary driver. The costs are being shouldered almost entirely by working tax payers.

Where does this leave us as consumers of health care? Specialty drugs are targeting roughly 2% of the population yet are projected to account for 50% of the overall costs. A few of the questions we must grapple as a society are:

“At what point does health insurance become so unaffordable or deductibles are so high that people forego medically necessary treatments because they simply cannot bear the cost of insurance or their portion of the overall costs?”

“Most of us are fine with limiting expensive treatments for everyone else. What if one of those treatments would extend the life or quality of life for our spouse or child?”

“If an employer is faced with the prospect of dropping medical insurance for all of its employees versus eliminating specific drugs or procedures that none of its employees may rarely use in order to make the coverage affordable, does that make them a poor employer to work for or socially irresponsible?”

These are some tough questions we will need to deal with as a society.

While there are no clear or immediate solutions don’t expect congress to act on anything dramatic. There are currently 1,266 registered lobbyists in Washington, D.C. representing the pharmaceutical industry. With 100 U.S. Senators and 435 U.S. Representatives, one of these lobbyists could take a congressman to lunch every day of the year and a Representative or Senator would never see the same lobbyist twice in over years. The only thing that seems to get a congressman’s attention is a ground swell of complaints because getting re-elected is paramount to their legislative career.

A solution to the exponential health care costs needs to be devised soon. Other than eliminating expensive drugs and procedures from medical plans there doesn’t seem to be any solutions on the horizon. Perhaps it’s time for all of us to decide what we can afford as a society and raise the voice of concern to all who will listen.

This blog was written by Scott Deru, RHU, REBC, President of Fringe Benefit Analysts, LLC®, an employee benefit consulting firm providing benefit solutions for firms throughout the country. Scott is a Registered Health Underwriter and Registered Employee Benefit Consultant and is currently Vice Chairman of the Board of United Benefit Advisors, an international partnership of premier benefit advisors.